Many accountants falsely believe that there’s only one standard that deals with long-term tangible assets: IAS 16 Property, Plant and Equipment.

While it’s true that you need to apply IAS 16 for most of your long-term tangible assets, it’s not the one ruling all. I tried to falsify this myth some time ago here.

Except for IAS 16, we have a few other standards arranging the long term assets. IAS 40 Investment Property is one of them.

In today’s article, you’ll learn:

Here’s a little bonus for you:

Before we dive in IAS 40, my good friend Professor Robin Joyce wrote a wonderful piece that teaches you accounting for IAS 40 in 40 seconds. Hope you’ll enjoy!

Special For You! Have you already checked out the IFRS Kit ? It’s a full IFRS learning package with more than 40 hours of private video tutorials, more than 140 IFRS case studies solved in Excel, more than 180 pages of handouts and many bonuses included. If you take action today and subscribe to the IFRS Kit, you’ll get it at discount! Click here to check it out!

The accounting for IAS 40 Investment Property is identical to that of IAS 16 (Property, Plant and Equipment),

EXCEPT

that IAS 40 revaluations (both positive and negative) go to the income statement (not revaluation reserve)

AND

there is no depreciation if revaluations are carried out every year.

DONE!

Any remaining seconds should be spent on learning the classifications and rules of IAS 40 Investment Property.

Now, let’s take Robin’s advice and spend the remaining seconds for learning the rest.

IAS 40 Investment Property prescribes the accounting treatment and disclosure with respect to investment property.

But, what is investment property?

The investment property is a land, a building (or a part of it), or both, held for the following specific purposes:

Here, the strong impact in on purpose. If you hold a building or a land for any of the following purposes, then it cannot be classified as investment property:

If you’re using your building or land for the first 2 purposes, then you should apply IAS 16; and the standard IAS 2 Inventories fits when you use them for the sale in ordinary course of business.

What specifically can be classified as investment property?

Here is a couple of examples (refer to IAS 40.8):

The rules for recognition of investment property are essentially the same as stated in IAS 16 for property, plant and equipment, i.e. you recognize an investment property as an asset only if 2 conditions are met:

Investment property shall be initially measured at cost, including the transaction cost.

The cost of investment property includes:

You should NOT include:

When payment for investment property is deferred, then you need to discount it to its present value in order to set the cash price equivalent.

Let me just mention that actually, you can classify assets held under the lease as investment property and in this case, it’s initial cost is calculated in line with IFRS 16 Leases.

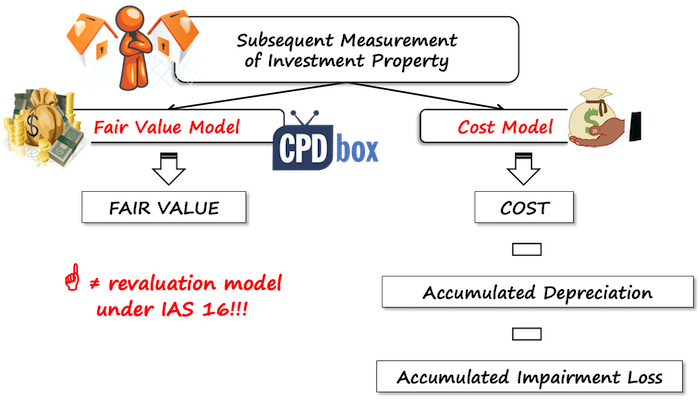

After initial recognition, you have 2 choices for measuring your investment property (IAS 40.30 and following).

Once you make your choice, you should stick to it and measure all of your investment property using the same model (there are actually exceptions from that rule).

Under fair value model, an investment property is carried at fair value at the reporting date. (IAS 40.33)

The fair value is determined in line with the standard IFRS 13 Fair Value Measurement.

A gain or loss from re-measurement to fair value shall be recognized in profit or loss.

Sometimes, the fair value cannot be reliably measurable after initial recognition. This can happen in absolutely rare circumstances (e.g. active marked ceased existing) and in this case, IAS 40 prescribes (IAS 40.53):

The second choice for subsequent measurement of investment property is a cost model.

Here, IAS 40 does not describe it in details, but refers to the standard IAS 16 Property, Plant and Equipment. It means you need to take the same methodology as in IAS 16.

Can you actually switch from cost model to fair value model or vice versa from fair value model to cost model?

The answer is YES, but only if the change results in the financial statements providing better, more reliable information about company’s financial position, results and other events.

Special For You! Have you already checked out the IFRS Kit ? It’s a full IFRS learning package with more than 40 hours of private video tutorials, more than 140 IFRS case studies solved in Excel, more than 180 pages of handouts and many bonuses included. If you take action today and subscribe to the IFRS Kit, you’ll get it at discount! Click here to check it out!

Switching from cost model to fair value model would probably meet the condition and therefore, you can do it whenever you’re sure that you’ll be able to determine the fair value regularly and the fair value model fits better.

However, the opposite change – switch from fair value model to cost model – is highly unlikely to result in more reliable presentation. Therefore, you should not really do it, and if – rarely and for good reasons.

When we speak about transfers related to investment property, we mean the change of classification, for example, you classify a building previously held as property, plant and equipment under IAS 16 to investment property under IAS 40.

The transfers are possible, but only when there’s a change in use or asset’s purpose, for example (refer to IAS 40.57):

What’s the accounting treatment in this case?

It depends on the type of a transfer and the accounting choice for your investment property.

If you opted to account for your investment property at cost model, then there’s no problem with the transfers, you simply continue with what you did.

However, if you picked up a fair value model, then it’s a bit more complicated:

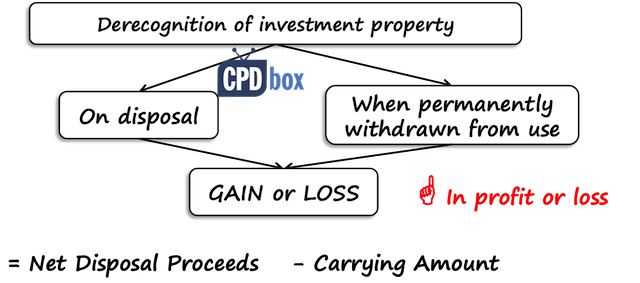

The derecognition rules (=when you can remove your investment property from your books) in IAS 40 are similar to the rules in IAS 16.

You can derecognize your investment property in two circumstances (IAS 40.66):

You need to calculate gain or loss on disposal (IAS 40.69) as a difference between:

Gain or loss on disposal is recognized in profit or loss.

IAS 40 Investment property prescribes a lot of disclosures to be presented in the financial statements, including the description of selected model, how the fair value was derived, what the classification criteria for investment property are, movements in investment property during the reporting period (please refer to IAS 40.74 and following for more information).

Please watch the following video with a summary of IAS 40 Investment property: